After Federal Reserve Chair Jerome Powell’s recent speech at the Jackson Hole Economic Symposium, it is all but certain that the Fed will begin to reduce the fed funds interest rate in September, with most market prognosticators looking for a reduction of 0.25%, possibly 0.50%.

For investors and homeowners, this should be viewed as a positive – lower interest rates are an economic stimulant. For existing homeowners, this means possibly refinancing their mortgages, thus lowering their monthly payments. Increased spending power from lower rates typically flows into additional goods and services, which would increase overall economic growth – something investors would rejoice.

But what if the Fed cuts rates and mortgage rates don’t decline, or what if mortgage rates decline but not enough for the average homeowner to take advantage? To answer these questions, it’s important to understand which interest rates drive mortgage rates and the extent to which a decline in mortgage rates can spark a stimulative refinancing wave.

When Can Homeowners Expect To Refinance After The Fed Starts Cutting Rates?

For existing homeowners and new home buyers, the prospect of lower mortgage interest rates is enticing. With the Fed expected to begin a rate-cutting cycle in September, homeowners and prospective buyers may also expect to see lower mortgage rates in September. Well, not so fast. The relationship between the Fed’s policy rate and mortgage rates is not a direct link and comes with a delay.

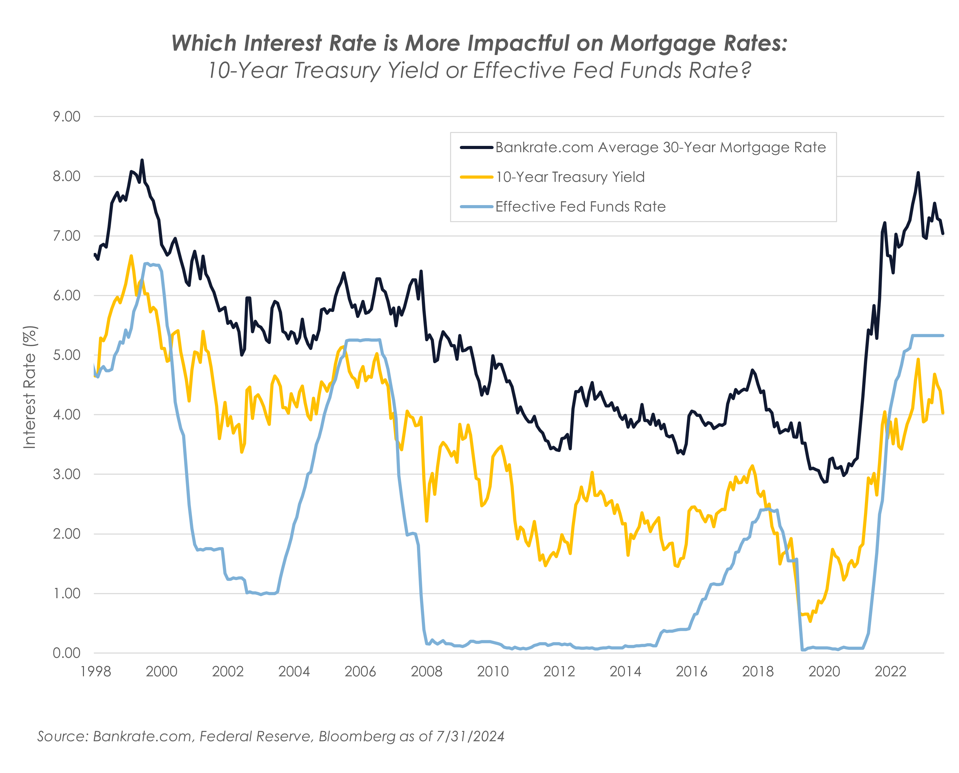

A good example was the timeframe from June 2004 to July 2006. During that period, the Fed increased interest rates by 4.25%, yet the average interest rate rose only 0.30%. Conversely, in response to the Great Financial Crisis in 2007 and 2008, the Fed slashed front-end rates by more than 5.00%, yet mortgage rates declined by only 1.02%.

A better gauge of when and by how much homeowners should expect mortgage rates to move would be to look at the yield on longer-term U.S. Treasuries instead of the fed funds rate.

The chart above shows that the correlation between the U.S. 10-year Treasury yield and the average mortgage rate is stronger than that of the fed funds rate. A regression analysis over the time period shown above results in a strong 86% R2 using the 10-year Treasury yield in comparison to a 66% R2 using the effective fed funds rate.

While a decline in the fed funds rate should eventually result in lower mortgage rates, homeowners and home buyers should not expect an instantaneous reaction and instead look toward the 10-year Treasury rate as a more reliable indicator.

When Can Investors Expect An Economic Boost From Refinancing?

Most homeowners who took out a mortgage in the last decade are feeling pretty good about their rate. When the topic of conversation turns to mortgages, they will gladly tout the low interest rate they locked in compared to where rates are currently. It has become a parlor game, with the winner being the borrower with the lowest mortgage rate.

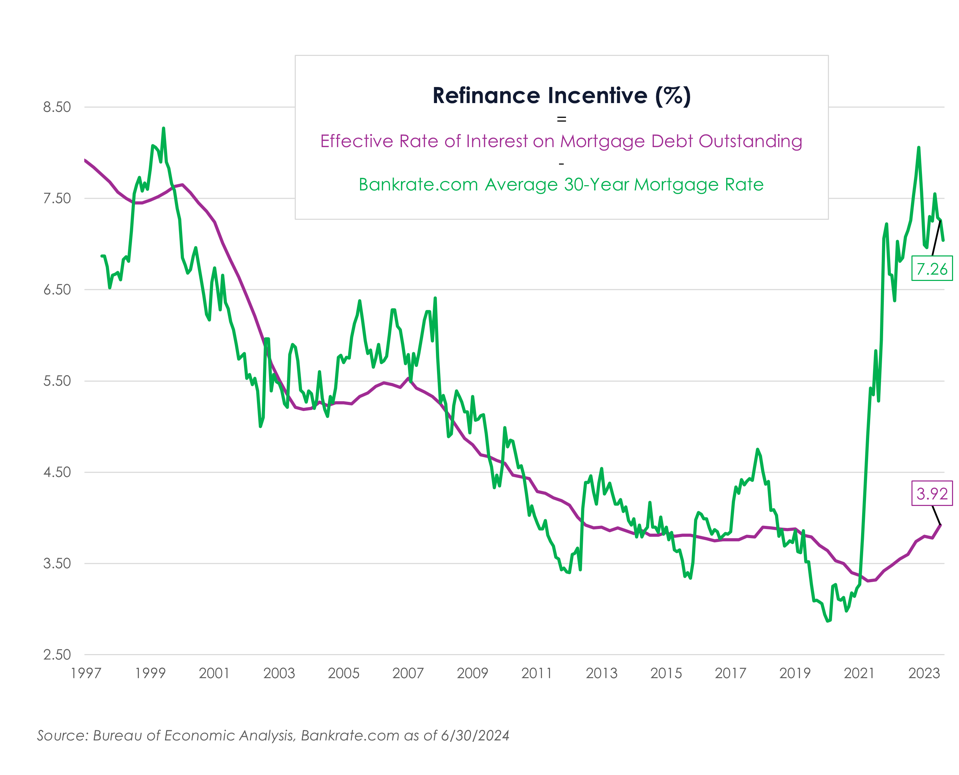

With this in mind, let’s gauge the likelihood and strength of a potential refinance wave. To do so, it’s useful to examine the relationship between the average consumer’s outstanding mortgage rate and current available mortgage rates.

According to the most recent data from the Bureau of Economic Analysis, the effective rate of interest on U.S. mortgage debt outstanding is 3.92% as of June 30. Compare this to the average mortgage rate as represented by the Bankrate.com average 30-year mortgage rate of 7.26%, also as of June 30, and the result is a negative refinancing incentive of -3.34%, near historic lows. These three measures are reflected in the two charts below.

Since early 2022, the calculated refinance incentive has been negative, which means the average … [+]

Fidelis Capital

The current mortgage rate would need to fall significantly before the average homeowner stands to … [+]Fidelis Capital

Investors looking for an immediate boost to the economy as a result of lower mortgage rates may be disappointed. While some borrowers may be able to take advantage of a small decline in mortgage rates, the vast majority still face a large negative incentive. Even if the expected 0.25% to 0.50% fed funds rate reduction in September were applied instantaneously to a reduction in mortgage rates, a large majority of homeowners would still not be able to benefit.

That said, the mortgage rate market is heading in the right direction. In October 2023, mortgage rates hit a 23-year high of 8.09% before declining to 6.86% as of August 21. Additionally, the average interest rate on outstanding mortgages has been on the rise after hitting a low of 3.31% in March 2022. Both metrics are moving in the right direction to facilitate a stimulative refinancing wave, though it will be some time until we see a meaningful impact.

The Bottom Line: Rate Cut Benefits Are On The Horizon But Not Here Today

For homeowners and home buyers, when the Fed begins cutting the fed funds rate this year and into next year, don’t expect mortgage rates to follow in lockstep. Instead, look to changes in longer-term Treasury market rates for clues as to how much and how quickly mortgage rates could move. And for investors looking for lower mortgage rates to boost economic growth, the current high rates will have to come down significantly before a meaningful impact will be observed. Both investors and homeowners will eventually benefit, but it may take longer than some expect.